The meteoric rise of quick commerce, promising deliveries in minutes rather than hours or days, is undoubtedly redefining consumer expectations and convenience. However, a recent report from global consulting firm Kearney issues a significant caution: this rapid growth is increasingly cannibalizing sales from other established retail channels, posing a complex challenge for the broader retail ecosystem, including traditional brick-and-mortar stores and even conventional e-commerce.

Quick commerce, or "q-commerce," typically involves ultra-fast delivery of groceries, daily essentials, and increasingly, a wider range of products, often within 10 to 30 minutes. This model thrives on strategically located dark stores or micro-warehouses and advanced logistics networks. While consumers are embracing the unparalleled speed and convenience, the Kearney report highlights the unintended consequences for other retail formats.

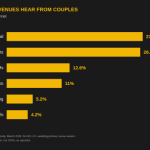

The report suggests that the swiftness of q-commerce is directly siphoning off sales, particularly for spontaneous, emergency, and emotional purchases. Consumers, increasingly accustomed to instant gratification, are turning to quick commerce for items they might have previously bought from a local kirana store, a supermarket, or even placed as part of a larger, less urgent online order. This shift is creating internal competition within the retail landscape, where quick commerce platforms are, in effect, "eating" into the sales of their own or partner companies' other channels.

For traditional retail, the impact is becoming profound. Kirana stores, which have historically been the backbone of Indian retail due to their proximity and convenience, are particularly vulnerable. Reports indicate that a significant percentage of quick commerce users have reduced their purchases from kirana stores, with some even stopping altogether. This is due to quick commerce's ability to offer competitive prices (often subsidized by heavy venture capital funding) and a level of speed that traditional stores cannot match for many common items.

Even established e-commerce players are feeling the ripple effect. While quick commerce is a subset of e-commerce, its ultra-fast delivery model differentiates it. Traditional e-commerce, with its longer delivery times, might lose out on impulse buys and immediate needs to q-commerce platforms. This compels larger e-commerce players to either acquire or develop their own quick commerce capabilities, further blurring the lines between channels and intensifying competition.

The Kearney report emphasizes that while quick commerce offers significant benefits in terms of convenience and efficiency, the long-term viability of its business model and its broader impact on the retail landscape need careful consideration. The challenge for retailers is to integrate quick commerce into an omnichannel strategy without inadvertently undermining their existing, often profitable, channels. This could involve strategic partnerships, developing specialized quick commerce offerings for specific product categories, or rethinking the role of physical stores as experience centers rather than just transactional points.

For startups in the retail technology and logistics space, this dynamic presents both challenges and opportunities. There's a growing need for solutions that help traditional retailers adapt to the quick commerce wave, perhaps by optimizing their own last-mile delivery or integrating with q-commerce platforms more effectively. The report underscores that quick commerce is not just a passing fad; it's a fundamental shift in consumer behavior that will continue to remodel the retail industry for years to come. Retailers and startups alike must strategize carefully to navigate this evolving landscape and harness the potential of instant gratification while mitigating its cannibalistic tendencies.